What is TDS - Tax Deduction at Source

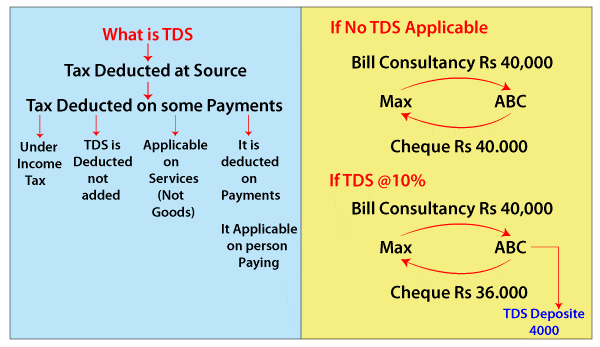

TDS refers to the tax deducted at the source. In order to collect tax at the source, TDS was introduced.

The tax is deducted at the source by a person (deductor) who is required to make certain payments (deductees) and remits the money to the Central Government.

According to the Form 26AS or TDS certificate given by the deductor, the person from whom income tax has been collected at the source is eligible to get a refund for the balance thus withheld.

In simple words, TDS is a source or a method to collect tax on income, dividends, and asset sales. The payer (or legal intermediary) must subtract the tax payable before delivering the remainder to the payee (and the tax to the revenue authority). According to the Income Tax Act of 1961, income tax must be levied at the source.

Any payments covered by these rules must be made after a defined proportion of income tax has been deducted from the payout.

Central Board for Direct Taxes (CBDT) manages it, and the Indian Revenue Service administers it as part of the Department of Revenue.

Goals of TDS

Tax Deducted at source has various benefits and objectives; these can be listed as follow;

- To allow salaried workers to pay their monthly taxes in accordance with their monthly earnings.

- This allows salaried individuals to pay their taxes in convenient monthly instalments, avoiding the pressure of a large payment.

- For contractors, professionals, etc., to gather the tax at the moment of disbursement of their income.

- Throughout the year, the government is in need of financial assistance to meet its obligations. Deduction at source as well as advance taxes allows the government to receive funds throughout the year, allowing it to function efficiently.

TDS Certificates

Certificates of compliance with the TDS include;

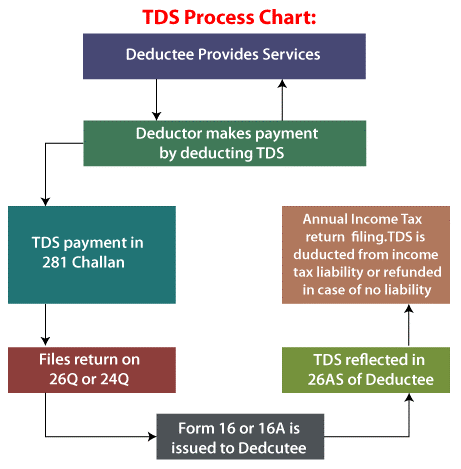

For paid employees, the deductor must issue a TDS certificate called Form 16 within a set period of time, and for non-salaried workers, Form 16A.

It is a TDS Certificate issued by the payer for commission, brokerage, contractual fee, and professional fees paid under section 194M of the Internal Revenue Code.

There is a 5-percent tax deduction requirement under Section 194M for payments to resident contractors and professionals that exceed INR 50,000,000 in a Financial Year.

TDS Certificates are to be issued within two months of the start of the next financial year by the deductor.

TDS has two major types of forms:

Form 16

- An employer must fill out Form 16 to declare the individual employee's wage and TDS deducted for the year.

- Part A and Part B of Form 16 are separate documents.

- It contains information about the company's and the worker's names and addresses, as well as their PAN and TAN numbers, employment dates, and TDS deducted and deposited with the government.

- Included in Part B are information on salaries and incomes, as well as deductions and tax payables.

Form 16A

- In addition to being a TDS certificate, Form 16A is also appropriate to TDS on earnings other than salary.

- On this certificate, you will find information such as the name, address, and PAN/TAN of the deductor or deductee, as well as the amount of TDS that was deducted and submitted. Form 26AS will retrieve information from Form 16A.

The Method of TDS Collection

There are two modes by which TDS can be collected.

Taxes subtracted or collected at source must be transferred to the account of the Central Government using one of the following methods:

1) The first mode is electronically

E-payment or electronic/ digital payments are required for

a) All company evaluations; and

b) All assessments (other than corporations) to whom the provisions of Section 44AB of the Income Tax Act of 1961 apply.

2) The other mode of deduction or collection of TDS is the Physical mode

In this, the TDS can be subtracted by presenting the Challan 281 to an authorised bank branch.

Also, it is essential to note that: It is possible for a government office to remit income tax without producing an income-tax challan when tax is deducted or collected.

Any individual (be it an accounts officer, treasurer, or disbursing officer )to whom a deductor notifies the tax subtracted and who is accountable for transferring the amount to the Central Government shall issue a statement in Form No. 24G to NSDL within the statutory timeframe.

Tax deductibility rates

Rates for tax deductions are set forth in the applicable statutes or the First Schedule to the Finance Act.

The holding tax rates stipulated in the Double Taxation Avoidance Agreements, however, must also be taken into account when payments are made to non-residents.

TDS Dividends

By-law section 302 of the Indian income tax act (1961) makes this point.

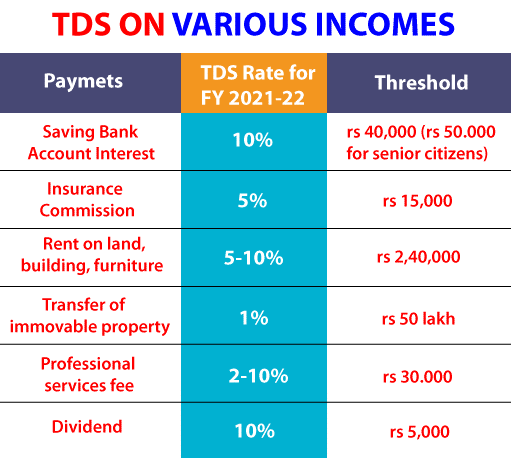

- Dividend income was tax-free in the ownership of the shareholder prior to Budget 2020. Dividend income in excess of INR 5000 is subject to TDS @ 10% u/s 194 as of Budget 2020.

- This section only applies to presumed dividends u/s 2(22)(e) that exceed 2500 per year.

- The tax rate on such dividends is 1 percent.

- SADHA, GIC(General Insurance Corporation), its subsidiary, or any other insurer that owns or has a complete beneficial interest in shares will be exempt from the provisions.]

Section 115-O dividends are exempt from this deduction.

- Non-filers of income tax returns pay much higher TDS charges.

TDS or Tax Deduction At Source in case of Immovable Property

- 1961's Income Tax Act Section- 194IA.

- Transactions occurring on or after June 1, 2013, are subject to this rule

- Certain immovable property other than agricultural land is to be taxed at source when transferred to a resident.

- As a transferee, every individual who must pay more than 50 lakhs in consideration for the transfer of immovable property is required to deduct 1 percent tax at the source.

It is essential that this TDS on real estate be deposited within 30 days of the month in which it is deducted for all transactions made on or after 1 June 2016.

2. The 1961 Income Tax Act section 194IB

- Transactions occurring on or after June 1, 2017, are subject to this rule.

- Individuals or HUFs who pay rent to a resident landowner amount more than Rs. 50,000 per month would have tax deducted at the source.

- TDS shall be deducted at 5 percent at the moment of crediting rent for the endmost month of the last year or the endmost month of the lease if the premises is deserted during the year.

3. Section 194C of the 1961 Income Tax Act.

- Contractors and subcontractors are required to deduct 1 percent (for individuals, HUF) or 2 percent (for others) of any payment made for the performance of any job (including the provision of labour for the performance of any work and advertisements).

- A contract (including a subcontract) between the contractor and payer must govern such work.

- Payments in cash, via check, drafts, or any other means of payment must be made with TDS deductions at the instance of crediting to the contractor's account and/or at the time of payment.

- As long as the contractor receives no more than Rs. 35,000 or Rs. 1,000,000 in one year, no TDS will be deducted.

Conclusively, the following forms of transactions are subject to TDS:

Salaries; Interest by the bank; Commission payment; Rent Payment, Consultation fee; Professional fee.

Tax deducted at source (TDS) is not required by individuals when making rent payments and paying fees to the professional such as attorneys and doctors.

As an example, TDS is a form of advance tax. Taxes must be submitted with the govt on a regular basis, and the deductor has the responsibility of doing so on time/promptly. The deductee can claim a tax refund for the TDS deducted after filing their ITR.

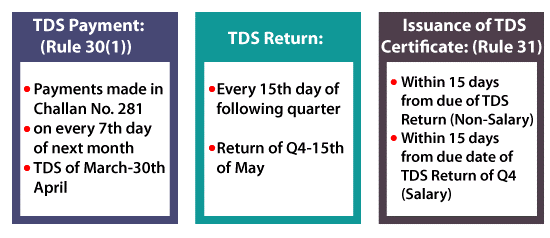

TDS Return

In addition, the deductor must file a TDS return in order to report the information of the deducted TDS to the government. Quarterly TDS returns must be filed. Diverse TDS return forms are required for various types of TDS deductions.

Non-compliance with TDS

No compliance with the TDS Income Tax Act of 1961 has negative consequences.

There are various acts and laws that can be imposed depending on the type of non-compliance.

These Acts include;

- Disallowance under section 40(a)(ia) of the Income Tax Act of 1962. (Act)

- Section 201(1) of the Act provides for an increase in demand.

- Section 1A of the Act allows for interest to be charged.

- Section 271C of the Act imposes a penalty.

- If there is failure to deduct TDS- He/She is liable for interest at the rate of 1 percent per month from the date the tax was due to the date it was deducted if TDS was not deducted from the payment on time or as required.

- To the extent that a person fails to deduct the entire amount of tax he is required to deduct, he may be penalised by a Joint Commissioner up to an amount equivalent to that amount of tax, as per Section271C of the Income Tax Act.

- If there is failure to pay TDS- Under Section 201 of the Income Tax Act, an individual who fails to pay the amount of TDS deducted from a payment they are making to a resident is subject to a 1.5 percent interest charge per month or part of a month from the date it was deducted until the date of payment.

- Tax arrears are subject to a maximum penalty for non-payment under section 221, which allows the Assessing Officer to order a person to pay the amount of TDS deducted at source from payment if he or she does not pay it. Before imposing the penalty, the person will have a sufficient chance to be heard.

- If there is a default in filing of return- Failure to file a return on time does not result in an interest penalty. However, he must pay Rs. 100 per day for each day he fails to file his TDS return in accordance with the Act, up to the maximum of his TDS liability.

Non-compliance with TDS rules may have additional repercussions, including Disallowance of Expenditure and Prosecution.

- According to section 139(1) of the Income Tax Act, a person who makes a deduction of TDS while paying a resident can claim the payment as an expenditure.

- Under section 40(a)(ia), if a person fails to deduct the required amount of TDS or deducts it but fails to pay it, the full amount deducted is disregarded for computing income under the "PGBP" heading.

- Assesses who have deducted tax at source and do not pay it to the government within a specified time frame may be punished with a sentence of harsh imprisonment under section 276B of the Income Tax Act: a period of not less than three (3) months.

However, it may last up to seven years if the fine is included.

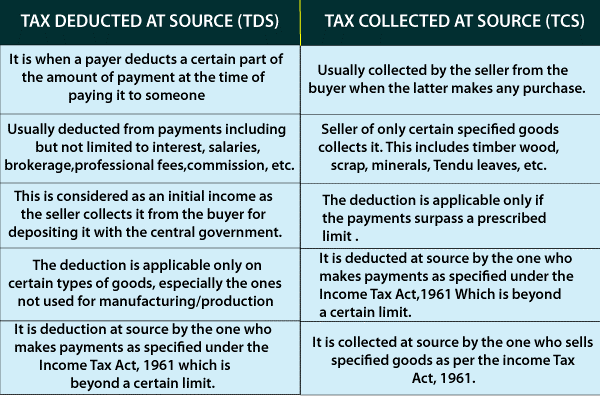

Tax Deductor vs. Tax Collector

- The tax collector must get the tax collection account number from the tax collection agency. It will be necessary for the tax deductor to obtain a tax deduction account number.

- Every document relating to TDS/TCS must contain the tax number that was obtained (as applicable).

- In addition, the tax collector must be aware of and collect tax at the rate that is in effect throughout the specified time period.

- In order to deduct taxes, the tax deductor will need to follow the same steps.

- Taxes that have been collected and deducted must be credited to the Central Government by the deadlines stated.

- Periodic TDS/TCS returns and TDS statements must be filed on or before the due periods prescribed in the Income Tax Act of 1961.

- TCS and TDS certifications are sent to the buyer and the payee before the required dates for filing income tax returns.

Non-payment of taxes by tax deductors and tax collectors has various repercussions.

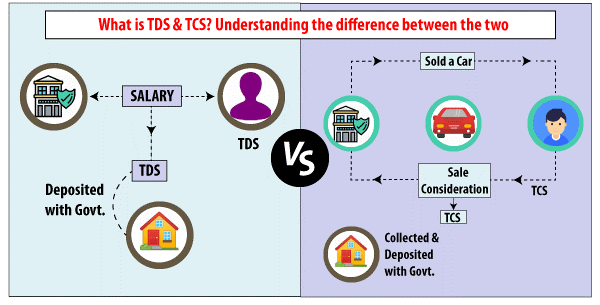

Unlike TDS, where the tax is deducted at the time of payment, TCS collects the tax from the customer. TCS is a method of tax collection for defined commodities that are used to collect taxes. The individual whose income is taxed, as well as the person whose purchasing expenses are taxed, both gain from the tax. TDS/TCS Credit is used to obtain this benefit.